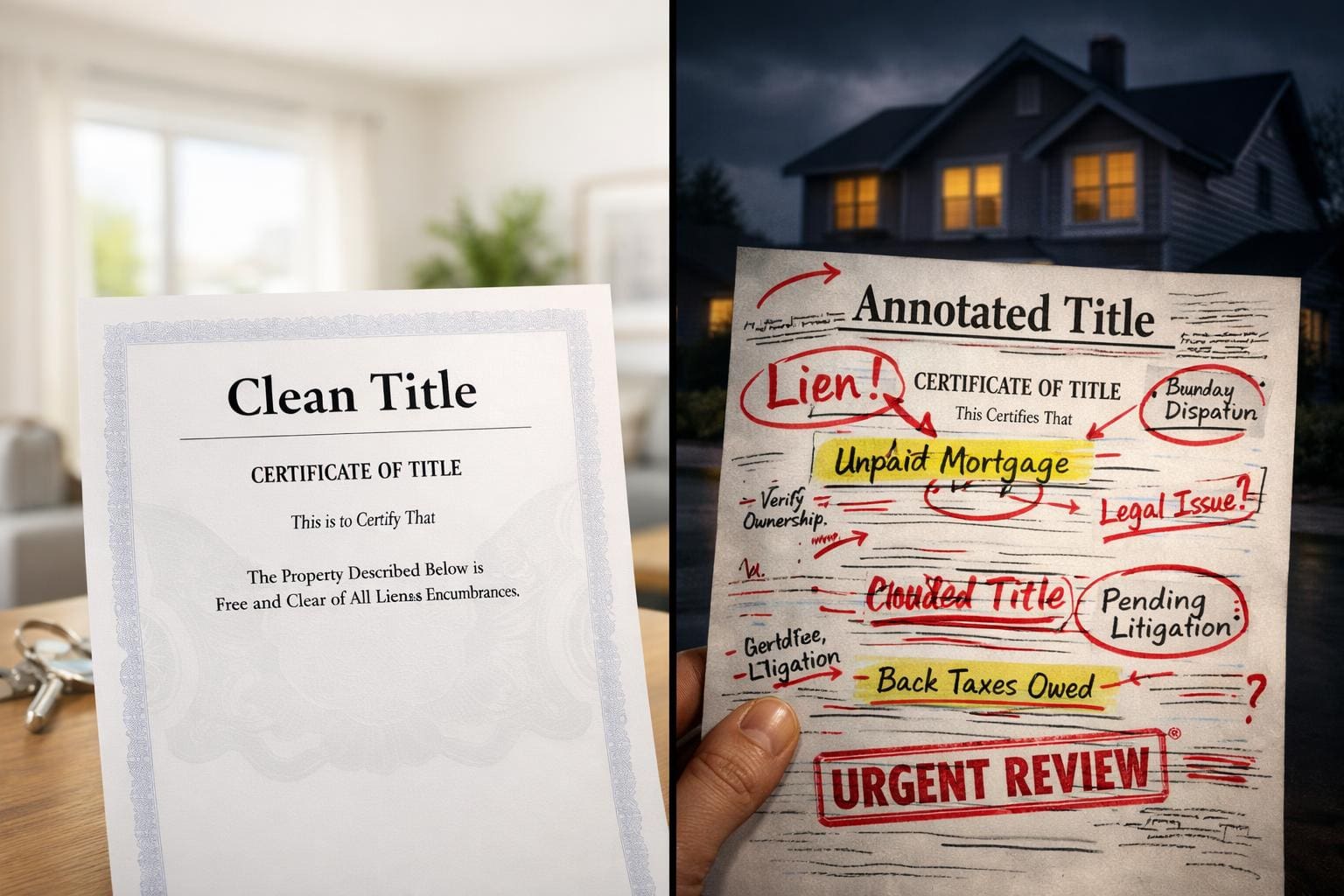

Annotated Title vs. Clean Title in the Philippines

When you’re buying property in the Philippines, the annotated title vs. clean title debate pops up almost every time. The certificate of title? That’s the big one. It’s the proof of who owns the land or condo unit, and it’ll show if there are any legal issues, liens, or third-party claims tied to the property.

If the title is “clean,” there are no annotations on the back. That’s a green light: the property can be transferred, financed, or resold without legal headaches. An annotated title, though, means there are notes—maybe obligations, restrictions, or even disputes. Not every annotation is a deal breaker, but every single one deserves a close look before you put your money down.

Annotations can be as simple as a mortgage note that’s erased once the loan’s paid, or as serious as an adverse claim or a pending court case, which can freeze the whole transfer. Honestly, sometimes your entire risk comes down to those back pages and whether you know what each scribble means.

This guide lays out the key differences, runs through common annotations, and gives a practical way to check titles. You’ll also get a sense of when to move forward and when to just walk away.

Key Takeaways

- A clean title has no liens or claims—usually the safest, and banks like it best.

- Annotated titles aren’t always bad, but every annotation needs to be checked, explained, and ideally cleared before you buy.

- Always verify the title at the Registry of Deeds and talk to a licensed professional. Seriously, don’t skip this.

What Buyers Need to Know First

There are three main types of property titles in the Philippines: Transfer Certificate of Title (TCT) for land, Condominium Certificate of Title (CCT) for condos, and Original Certificate of Title (OCT) for land that’s newly registered. Whether you’re eyeing a house in Talisay or a condo in Cebu IT Park, what matters more than the type is what’s scribbled on the annotation page. Clean and annotated titles come with different risks, transfer speeds, financing options, and resale possibilities.

What A Clean Title Usually Means

A clean title means those annotation pages are empty. No liens, mortgages, adverse claims, or weird restrictions. The seller owns it outright, and nobody else has a legal foot in the door.

For buyers, this makes life easier. Banks process loans faster. The Registry of Deeds doesn’t get bogged down. And if you sell later, it’s a breeze for the next buyer too.

Of course, “clean” doesn’t mean perfect. Things like unpaid taxes or even fake docs can still lurk in the background. But if the annotation page is spotless, that’s about as good as it gets to start with.

What An Annotated Title Signals

An annotated title has stuff written on the back of the TCT, CCT, or OCT. The Registry of Deeds puts these there to show something is up with the property.

Some common examples:

- Mortgage liens from banks

- Adverse claims—someone else says they own it

- Lis pendens—there’s a court case in play

- Easements or use restrictions

- Settlement notes from estate processes

Each annotation has its own story. Some are no big deal and can be cleared up. Others? Not so much.

Why An Annotated Title Is Not Automatically A Bad Purchase

Let’s say there’s a mortgage annotation. That doesn’t mean you should run. If the seller pays off the loan and gets the release from the bank before transfer, the annotation gets erased. It’s basically clean again.

In pre-selling developments, you’ll often see developer-related annotations. These are routine, especially in places like Cebu Business Park or Mandaue. Good agents see these all the time and know how to handle them.

The real question: can you get rid of the annotation before or during the sale?

The Fastest Way To Compare Risk, Transfer Ease, And Resale Impact

| Factor | Clean Title | Annotated Title |

|---|---|---|

| Legal risk | Low | Depends on the annotation |

| Bank financing | Usually fast | Can be slow or denied |

| Transfer speed | Normal | Sometimes a slog |

| Resale value | Holds up well | Can take a hit |

| Due diligence needed | Basic checks | Needs a deep dive |

If you’re a first-time buyer, a clean title is the safer bet. But if you’re a more seasoned investor and don’t mind doing your homework, sometimes annotated titles mean you can snag a deal—especially if the issue is minor and the price is right.

Common Annotations That Change the Buying Decision

The kind of annotation on a title can make a property either a manageable project or a legal headache. A mortgage annotation isn’t the same as an adverse claim or a lis pendens notice. Really, knowing what each annotation means—and how to clear it—is a must-have skill for property buyers here.

Real Estate Mortgage And Mortgage Annotation

A real estate mortgage (REM) annotation means the property was used to secure a loan. It’s super common, and, honestly, usually not a big deal.

If the loan is paid, the bank gives a release or cancellation of mortgage. The seller files this at the Registry of Deeds to wipe the annotation.

What to do: Check the loan balance, ask for proof it’s paid, and make sure the mortgage annotation gets cancelled before you buy. Don’t just take the seller’s word for it.

Adverse Claim And Third-Party Ownership Issues

An adverse claim means someone else thinks they have a legal right to the property. Maybe it’s a co-heir, a business partner, or a previous buyer who says the current sale isn’t valid.

This is a big red flag. Under Philippine law, adverse claims stay on the title for 30 days, but courts can extend that. While it’s there, it’s a warning: ownership is being challenged.

Buying with an active adverse claim? Risky. The claimant could block your transfer or drag you into court.

Lis Pendens, Notice of Lis Pendens, And Court Disputes

A lis pendens tells you there’s an ongoing lawsuit about the property. It doesn’t mean the owner’s lost the case, but the result could impact who owns it.

Properties with lis pendens? Approach with caution. Court cases here can drag on for years. During that time, you might not be able to sell, develop, or even mortgage the property.

Rule of thumb: Unless a real estate lawyer says the case is almost over and the seller will win, you’re probably better off looking elsewhere.

Easement, Right of Way, And Use Restrictions

An easement annotation gives someone else a limited right to use part of the property. A right of way, for example, lets a neighbor cross your lot.

Restrictions or declarations of restrictions limit what you can build or do. These are common in subdivisions and gated communities like Maria Luisa Estate, where rules cover building heights, setbacks, or business use.

Easements and restrictions usually stick around. They limit flexibility, but don’t always ruin a deal. Just make sure you read the details and see if it’ll cramp your plans.

Extrajudicial Settlement, Excluded Heirs, And Unpaid Creditors

If a property owner passes away, heirs sometimes do an extrajudicial settlement to split the property without court. This gets noted on the title.

The risk? If a rightful heir is left out, or if there are unpaid creditors, they can challenge the transfer later.

Ask for the settlement document, check if all heirs signed, and see if it was published in a newspaper as required.

Affidavit of Loss, Affidavit of Correction, And Other Red Flags

An affidavit of loss shows up when the owner’s duplicate title is reported missing. This starts the process to replace it, but it can also be a warning sign—sometimes it’s a cover for fraud if the “lost” title was actually sold or transferred without permission.

An affidavit of correction fixes typos or errors, like misspelled names or wrong lot numbers.

Other things to watch for:

- Attachments or levies from court judgments against the owner

- Missing marital consent, especially if it’s conjugal or paraphernal property

- Lots of annotations piling up—a messy ownership history

When the back of the title starts looking like a novel, it gets harder to finance, transfer, or resell. That’s when an agent who really knows the local scene can save you from a world of trouble.

How To Verify If the Title Is Safe To Buy

Title verification isn’t just a nice-to-have—it’s non-negotiable. The Philippine Supreme Court has made it clear: buyers need to dig deeper than whatever’s printed on the title. At the very least, you’ll want a certified true copy from the Registry of Deeds, a careful look at every annotation, and proof that taxes and transfer paperwork are in order. Skip a step, and you’re practically inviting trouble—fraud, transfer delays, or even losing the property entirely.

Check The Owner’s Duplicate Against Registry Of Deeds Records

The seller usually holds an owner’s duplicate certificate of title, while the Registry of Deeds keeps the original.

Ask for a Certified True Copy (CTC) from the Registry of Deeds, then compare it to the seller’s version. Double-check:

- Title numbers match

- Owner names and spellings are identical

- Lot and plan numbers line up

- Annotations are the same on both copies

If there’s a mismatch, don’t brush it off. It could mean tampering, fraud, or just an outdated duplicate—none of which you want to deal with.

In Cebu, the Registry of Deeds covers Cebu City, Mandaue, Lapu-Lapu, and nearby areas. Getting a CTC usually takes a few days.

Review The Annotation Page Line By Line

The back pages of a title list every annotation—dates, descriptions, sometimes a legal doc or case number. Go through each one and ask yourself:

- What exactly is this annotation?

- Is it still active, or has it been cancelled?

- Does it affect ownership, or just how the property can be used?

- Can it be sorted out before transfer?

Cancelled annotations should have a matching cancellation entry. If something’s still active with no sign of cancellation, it’s time to dig deeper.

Confirm Taxes, Transfer Documents, And Registration Requirements

Before you can transfer a title, a few things need to be squared away:

- Updated real property tax receipts—no unpaid taxes

- Certificate Authorizing Registration (CAR) from the BIR

- Deed of Sale signed by the right people

- Capital gains tax and documentary stamp tax paid up

If the seller can’t show these, or if taxes are overdue, expect delays. Build in extra time for tax clearances when planning your purchase.

Watch For Duplicate, Reconstituted, Or Overlapping Title Problems

Sometimes, a title is reconstituted—reissued because the original was lost or destroyed, maybe in a fire or typhoon. The process is legal, but it’s also a well-known loophole for fraudsters.

Overlapping titles—where more than one title claims the same land—are more common in the provinces, but they can crop up anywhere, especially in fast-growing areas.

Red flags to look for:

- Title annotated under Section 7 of R.A. No. 26 (reconstitution)

- Technical description doesn’t match the actual survey

- Two people both claiming the same lot with different titles

When in doubt, have a geodetic engineer verify boundaries and check with the Land Registration Authority to make sure the title’s legit.

Know When To Pause And Seek Legal Review

Sometimes, you just need to hit the brakes. If you see any of these, talk to a real estate lawyer before moving forward:

- Active adverse claims or lis pendens

- Missing or inconsistent annotation cancellations

- Reconstituted title with no court order

- Seller can’t show the owner’s duplicate

- Family disputes over the property

Working with licensed agents who know Cebu’s neighborhoods—say, from IT Park to Mactan—can help you spot these issues early. Cebu Grand Realty, for example, has verified listings and helps clients navigate title checks across thousands of properties.

When To Proceed, Renegotiate, Or Walk Away

Whether or not to buy a property with an annotated title really depends. What’s the annotation? Can the seller clear it? How much risk are you willing to take? The rules—Presidential Decree 1529, the Civil Code, the Family Code—set the framework, but real-world decisions hinge on context. Sometimes it makes sense to move ahead, sometimes not. There’s no one-size-fits-all answer, and honestly, a little caution never hurts.

When A Clean Title Is The Better Fit For Most Buyers

If you’re a first-time buyer or need a bank loan, stick with a clean title. Philippine banks almost always reject mortgage applications if the TCT or CCT has unresolved annotations.

Clean titles also make resale easier. Future buyers will do their own checks, and properties with simple, clear ownership histories are just more appealing.

If you want a hassle-free house, condo, or townhouse—especially in places like Cebu City or Talisay—go for clean titles. It’s just less stress.

When An Annotated Property Can Still Make Sense

Sometimes, buying a property with an annotation isn’t crazy. Two cases stand out:

- The annotation is routine and almost cleared. Maybe there’s a mortgage annotation with the release already in process, or a developer’s lien on a new condo that’s about to be lifted.

- The price makes up for the risk. If the property is way below market value because of an annotation—and a lawyer says it’s fixable soon—it might be worth the gamble.

Some investors in Cebu have picked up bargains in Mandaue or Lapu-Lapu where a simple annotation cancellation unlocked real value.

Conditions That Should Be Cleared Before Transfer

Before you sign anything, make sure these are sorted—or at least contractually guaranteed:

- All mortgage annotations have a release ready to file

- Adverse claims are withdrawn or dismissed by a court

- Lis pendens is lifted with a court order

- Certificate Authorizing Registration is secured from the BIR

- Marital consent is documented if required

If the seller can’t clear these, you might want to renegotiate the price to cover delays and legal costs—or just walk away.

Applying The Decision In Cebu Residential, Condo, And Commercial Deals

Cebu’s property market is a mixed bag. Buying a CCT in Cebu Business Park isn’t the same as picking up commercial land near Mactan.

For homes and condos, mortgage annotations pop up the most and are usually solvable. For commercial properties, you’ll want to pay closer attention to easements, deed restrictions, and zoning-related annotations—they can affect what you can actually do with the land.

Cebu Grand Realty’s agents have over 15 years of experience in Cebu City, Mandaue, Lapu-Lapu, Talisay, and nearby areas. They help buyers size up title conditions all the time. With more than 8,000 clients served, their local know-how on neighborhoods and trends is a real asset when reviewing annotations.

Honestly, a clean title is your safest bet. Only consider an annotated title if you fully understand the issue, know how to resolve it, and have a pro guiding you through the process.

Frequently Asked Questions

How can I verify whether a land title has annotations, and where should I request a certified true copy?

Ask for a Certified True Copy (CTC) of the title at the Registry of Deeds where the property is located. The CTC shows all annotations—active and cancelled. Always check that the CTC matches the seller’s owner’s duplicate.

What are the most common title annotations, and what does each one typically mean for a buyer?

You’ll usually see annotations like real estate mortgages (the property is collateral for a loan), adverse claims (someone else says they have rights), lis pendens (there’s a court case), and various easements or restrictions (limits on use). Each one has its own risk level—some are routine, others can kill a deal.

How does an existing mortgage annotation affect the sale, and what documents are needed to cancel it before transfer?

If there’s a mortgage annotation, the property is collateral for a loan. The seller has to pay off the loan and get a release or cancellation of mortgage from the bank. That document goes to the Registry of Deeds to clear the annotation before you can transfer the title.

Why do banks often hesitate to finance properties with annotations, and what factors can improve loan approval chances?

Banks see unresolved annotations as a legal headache—they might affect the property’s value or your ability to transfer it. Your mortgage application stands a better chance if the annotation is minor, about to be cancelled, or if the seller can prove it’ll be sorted before closing. Still, banks love clean titles best.

What due diligence steps should be completed before buying a property with an adverse claim or a pending court case?

Get a CTC from the Registry of Deeds, ask for court filings related to the adverse claim or lis pendens, and hire a real estate lawyer to check how strong the claim is and how long it might drag on. Don’t skip legal review here—otherwise, you’re risking your whole investment.

What are the practical risks of buying a property with an easement or restriction annotation, and how can it affect future use or resale?

An easement or restriction basically puts a limit on what you can do with your property. Maybe there’s a right of way, so other folks can cross your lot, or a deed restriction that says you can’t build above a certain height or run a business there. These things tend to stick around for good, and honestly, they can make the place less attractive to future buyers or box you in when it comes to what you can build or change down the line.

{kind=link}